True or false – you must have a social security number to qualify for a mortgage?

False!

Yes, you read that right. One common misconception about the homeownership process is that you cannot purchase a home without a social security number. For individuals who may not have a social security number, there is a path to home ownership called the ITIN Loan.

Using an ITIN number in place of a social security number allows immigrants to build equity, increase family stability, and enjoy the social and psychological benefits of home ownership. Keep reading to learn more about the ITIN Loan process and if it might be right for you.

Immigrants in the Mortgage Market

Contrary to unfortunate stereotypes, most non-citizens residing in the United States are fully participating in U.S. economic life. In fact, research indicates that between 50% and 75% of unauthorized immigrants pay federal, state, and local taxes, and many have Social Security and Medicare withheld from their paychecks.

Furthermore, estimates also suggest that immigrants are contributing billions of dollars to the economy through tax contributions and personal spending.

For many immigrants, home ownership is a dream, and a determining factor in their choice to live in the United States. And many immigrants do achieve this goal, with 3.4 million undocumented immigrants owning homes in the U.S.

However, considering their contribution to economic life, this is still a relatively small percentage of this immigrant population – roughly 31%, compared to 65.1% of the U.S. citizen population.

One reason for this disparity is confusion about whether those without social security numbers can qualify for mortgages, and fear that attempting to do so may result in legal consequences.

ITIN 101

Not everyone residing in the United States qualifies for a social security number. Typically, if you’re not a U.S. citizen and don’t have a Department of Homeland Security Work Authorization, you do not have a social security number – though you may eventually qualify.

These individuals are often referred to as “undocumented citizens,” even if they’re in the process of seeking legal status. In place of a social security number, these individuals may receive an Individual Taxpayer Identification Number (ITINs).

People can obtain an ITIN number by filing the IRS W-7 form. Some identifying documents will also be required, and may include a U.S. driver’s license, foreign driver’s license, birth certificate, medical records, Visa, National Identification Card, or U.S. Military Identification Card. After submitting the required information, the ITIN number is usually issued within 4 to 6 weeks.

Research indicates that, as of 2012, over 21 million individuals residing in the U.S. had been issued ITINs. Once assigned, this nine-digit number can empower the user to do much more than file taxes, including open a bank account, qualify for a credit card, or receive an EIN to open a business.

Moreover, an ITIN can allow an individual to legally purchase a home.

The ITIN Loan Application Process

Before moving on, let us address one common concern – some immigrants who wish to buy a home may worry that an ITIN mortgage lender will “report” them, or otherwise facilitate deportation.

Your mortgage lender only wishes to assist you in achieving your home ownership dream and, with your ITIN, you are legally eligible to engage in this process. Furthermore, your loan application is a confidential document and will not be shared with outside entities.

Additionally, buying a home is a wise choice for immigrant populations, allowing for a degree of financial security that is unobtainable on the rental market. And, as we’ll discuss, ITIN Loans are an excellent way to qualify for homeownership.

That said, these loans are a bit different than traditional mortgage loans.

Much like a traditional loan application process, you will need to verify that you have a steady form of income (usually for 2 years or more), and may be asked to provide several pay stubs to authenticate your wages. Your financial history is also important. You will likely be asked to provide banking statements that show your transaction history, and like other loan applications, a credit check will also be part of the process.

Often, you’ll need a minimum credit score of 600 to obtain the ITIN Loan. Additionally, you will be required to have filed two years of tax returns to qualify for an ITIN Loan. Lenders may also request your rental records and utility bills, plus a driver’s license or other photo identification.

And while much of what has been outlined so far may apply to other types of mortgage qualification processes, the ITIN Loan does have some slightly more challenging conditions, as well. For example, while a 43% debt-to-income-ratio is considered ideal for most conventional mortgage loans, an ITIN Loan usually requires a 50% debt-to-income ratio.

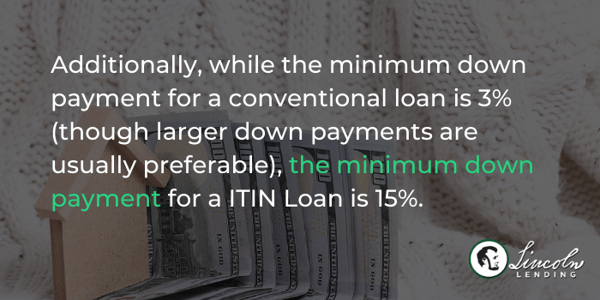

Additionally, while the minimum down payment for a conventional loan is 3% (though larger down payments are usually preferable), the minimum down payment for a ITIN Loan is 15%.

The interest rates of the ITIN Loans may not be quite as competitive as some other mortgage loans. However, interest rates are variable, and economic factors and personal considerations, such as credit score, can influence those rates.

Once you have successfully qualified for your loan, you should be able to purchase most types of conventional dwellings, including single family homes, condos, duplexes and townhomes as your primary residence.

Benefits of the ITIN Loan

One of the biggest benefits of the ITIN Loan is that it provides a pathway to homeownership for those who do not have a social security number. Homes purchased with ITIN Loans legally belong to their owners and cannot be repossessed due to a challenge to immigration status – though they can be foreclosed upon for nonpayment.

As a result, those who purchase homes with ITIN Loans are able to build equity, transfer homes to their children, and otherwise participate in the pride and stability of owning a home. Moreover, since many immigrant families enjoy the experience of living intergenerationally, home ownership provides a way to keep families together without the restrictions of rental occupancy.

Another advantage includes the fact that these mortgages, when provided by a reputable lender, are safe, secure, and legitimate. Too often, for fear of deportation, immigrants fall prey to loan-based scams, or “hard money” loans from unreputable individuals, rather than seeking support from established mortgage providers.

ITIN Loans provide a means to achieve homeownership without the risk of predatory lenders or con artists, allowing borrowers to live their dream, and protect their investment.

Closing Thoughts

The mortgage process can be intimidating, even for U.S. citizens. The excitement and confusion of the experience are only increased for many immigrants who are navigating American banking and housing regulations for the first time.

This can be even more complicated when English is not your native language.

But don’t worry, a compassionate and experienced ITIN Loan Officer can answer your questions and walk you through every step of the pre-approval process.

Furthermore, many of the Lincoln Lending Loan Officers are bilingual, so you’ll always understand the process and be a true partner in your home purchase.

Ready to learn more? Contact Lincoln Lending today, and let’s start your journey to homeownership!