While homeownership is a big decision and a serious responsibility, there is a common belief that buying a home is simply out of reach for many average Americans. In fact, a recent survey revealed that 57% of non-homeowners think it would be difficult to become homeowners in their current financial situation.

The statistic reflects widespread misconceptions about what it really takes to buy a home.

The mortgage pre-approval process considers a variety of factors, including a person’s financial history, credit score, work history, and down payment amount. Furthermore, there is more than one kind of mortgage, including government-backed mortgages for those rebuilding credit, and even ITIN mortgages, for those without social security numbers.

Essentially, regardless of where you find yourself today, with a little knowledge and planning, your dream of owning a home can become a reality.

In this article, we’ll look at some common misconceptions about the home buying process and share some ways that you can improve your chances of mortgage approval success.

Misconception 1: You Need a Down Payment of 20%

Many people believe that you cannot buy a home without a down payment of 20%. However, the median American home price in 2019 was roughly $226,800, which would result in a down payment of $45,360.

Raising such a large amount of cash would be nearly impossible for many first-time homebuyers.

Thankfully, it’s not always necessary.

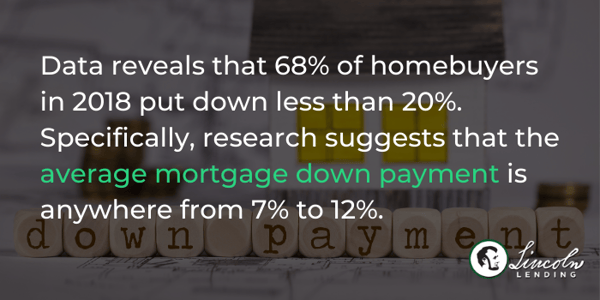

Data reveals that 68% of homebuyers in 2018 put down less than 20%. Specifically, research suggests that the average mortgage down payment is anywhere from 7% to 12%.

Moreover, some loans, such as Federal Housing Authority (FHA) loans, may require a down payment of only 3.5%, though they may also require mortgage insurance, burrower education, or other conditions.

How can you find out whether you’re eligible for these mortgage programs?

While internet research is a great place to begin learning about your options, we recommend seeking advice from an experienced mortgage lender. These professionals are familiar with a wide variety of mortgage programs and can guide you toward your best options for achieving your home buying goals.

Misconception 2: You Have to Have Outstanding Credit

Many people believe that they have to have “perfect” credit to purchase a home. In reality, a minuscule 1.2% of FICO scores are currently 850, and only 20% of the population have what is considered “excellent” credit.

So, what’s the significance of a credit score?

Credit scores fall in a range between 300 to 850 points and are used by lenders to evaluate your overall financial behaviors.

The following is a breakdown of how banks and lenders typically assess credit scores:

- Excellent: 800 to 850

- Very Good: 740 to 799

- Good: 670 to 739

- Fair: 580 to 669

- Poor: 300 to 579

Your payment history, outstanding debts, length of credit history, and the number of credit accounts are considered in the calculation of this score. And, since anyone can make a mistake, most lenders do not expect flawless credit.

Instead, for conventional loans, you usually need a credit score of at least 620, though a score of 740 or higher may help you qualify for the best interest rates. Furthermore, FHA loans are typically available for those with credit scores of 580 with a 3.5% down payment. People with a credit score of 500 may even be able to qualify if they can save up a 10% down payment.

This is not to say that credit scores don’t matter.

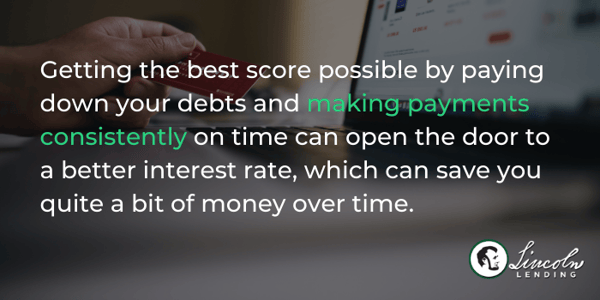

Getting the best score possible by paying down your debts and making payments consistently on time can open the door to a better interest rate, which can save you quite a bit of money over time. However, waiting for credit score perfection is not necessary. Wasting money on rentals in pursuit of flawless credit may be holding you back from investing in the home of your dreams.

Misconception 3: You Can’t Have Debt

Closely related to the misconception that home buyers must have perfect credit is the idea that they cannot have debt while qualifying for a mortgage.

This is simply not true.

When it comes to debt in the home buying process, the adage “everything in moderation” holds true. To this end, lenders carefully assess your debt-to-income ratio to put your debt into a larger context. Debt-to-income (DTI) ratio is calculated by adding up your mandatory monthly expenses, such as car payments, credit card payments, child support, rent, etc. (but not groceries, gas, childcare, or clothes). Once you have your expense total, you divide it by your monthly income before taxes to get your DTI ratio.

Most conventional mortgage lenders look for a debt-to-income ratio of 43% or lower. For example, if your monthly income is $3,500 before taxes, and you spend $1,300 each month on your rent, car payment, and credit card debt, your debt-to-income ratio would be 37%. This ratio would be adequate to qualify for many mortgage programs.

Keep in mind that paying down your debt, which improves your debt-to-income ratio and credit score in the process, is always a great idea. The stronger your financial situation, the better mortgage terms you will likely receive.

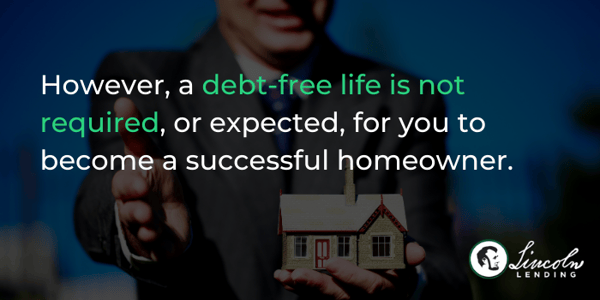

However, a debt-free life is not required, or expected, for you to become a successful homeowner.

Misconception 4: You Can’t Buy a Home Alone

Likely because of the misconceptions above, many single people do not believe that they can afford a home – or do not think it makes sense to purchase a home until marriage.

Only 38% of home buyers are single, yet the median age of first marriage in America is now nearly 30 years old. This means that many men and women miss out on the financial and psychological benefits of homeownership well into their adult years.

As they wait, they may be wasting money on rent or wasting time on less stable living situations. However, as we’ve seen, single people do not need to wait until they receive the benefit of a second income in order to begin building equity and enjoying greater stability.

Why wait another day?

Misconception 5: All Lenders Are the Same

There is often confusion regarding what constitutes a “mortgage lender,” with many people thinking that only banks can provide a mortgage loan.

There are advantages to obtaining a mortgage loan through a bank. For example, banks have the benefit of offering a number of financial services, such as checking and savings accounts, as well as investment brokers and financial planners, if needed. This can allow the borrower to bring all their banking under one roof, and individuals may feel comfortable with the staff at their local bank, due to previous interactions.

However, since banks offer so many services, they are not entirely dedicated to the provision of mortgages, and their staff may not have in-depth familiarity with all mortgage products on the market.

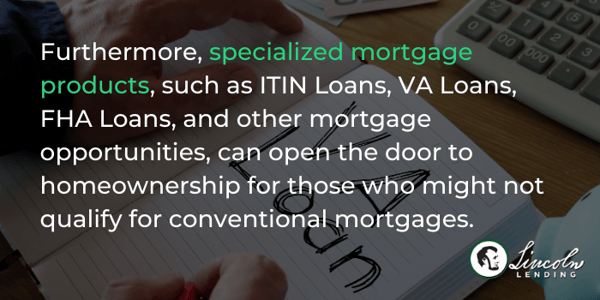

Furthermore, specialized mortgage products, such as ITIN Loans, VA Loans, FHA Loans, and other mortgage opportunities, can open the door to homeownership for those who might not qualify for conventional mortgages. A dedicated mortgage expert, such as might be found at a mortgage lending company, would be aware of these exciting opportunities, and more.

Additionally, mortgage lending institutions exist only to offer real estate loans and may conduct loan processing, underwriting, and closing functions internally, reducing wait time and confusion for the borrower. These institutions are also highly regulated, offering safe, secure, and confidential financial interactions.

Considering their expertise and dedicated focus, it makes sense to reach out to a reputable mortgage lending company as soon as you begin to consider homeownership.

In partnership with your lender, you may be able to identify different loans that could meet your needs, as well as a plan to maximize your opportunities. These experts will help you dispel myths, understand your financial strengths, and bring your homeownership vision to life.

Are You Ready to Own a Home?

If you’re ready to take your financial future into your own hands, get in touch with Lincoln Lending today. We’re passionate about homeowner education, and we’d love the opportunity to discuss these misconceptions and more to help you understand what it really takes for you to own your dream home.