As you begin your home buying journey, you’re probably asking yourself, “How much money should I borrow?” The answer to this question will determine which neighborhoods you should house hunt in and which homes you should consider, so it’s one that you should answer for yourself early on in your journey.

The good news? There are many free tools that can help you ballpark your budget. If the results are not what you expected, then try one of our tips to increase the loan amount that you qualify for.

Use a mortgage calculator

Are you curious about how much money you can borrow with your current income and debt levels? Would you like to know how much a $200,000 mortgage actually costs each month? Wish you could see how your loan qualification would change if you reduce your debt before applying? Try using a mortgage calculator!

A mortgage calculator is a quick and easy way to simulate how much you may be able to borrow under different financial circumstances. Keep in mind that this is just a rough estimate, not a guarantee. However, it can help you set expectations and begin understanding what your homeownership costs could be. After you try out a calculator, get in touch with Lincoln Lending to get an even more accurate idea of how much you qualify to borrow.

What impacts the amount that I can borrow?

There are several factors that lenders look at when determining the amount that you qualify for, and it’s important to understand each of these factors and how they impact your ability to borrow. A few pieces of data your lender looks at are:

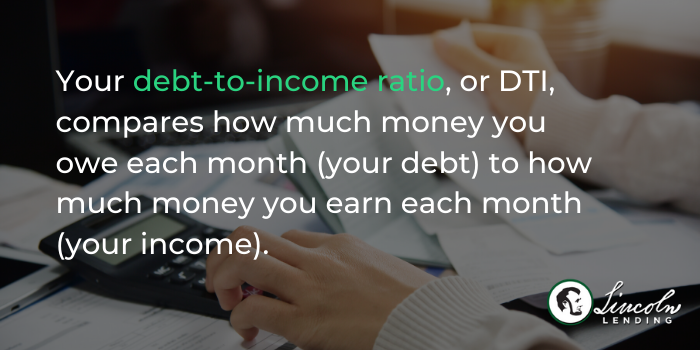

1. Debt-to-income ratio

Your debt-to-income ratio, or DTI, compares how much money you owe each month (your debt) to how much money you earn each month (your income). It includes debts like credit cards, rent, student loans, car payments, and other monthly obligations. A good rule of thumb is that the lower your DTI, the less risky you are to lenders, which means you may qualify for a better interest rate or higher loan amount.

2. Loan-to-value ratio

Your loan-to-value ratio is the amount of your mortgage compared to your property’s value, expressed as a percentage. For example, if you get a $70,000 mortgage to buy a $100,000 home, the loan-to-value ratio is 70%. A good rule of thumb is that you want your loan-to-value ratio to be below 80%. If your ratio is higher than 80%, you can still get a mortgage, but you will be required to purchase private mortgage insurance (Conventional loans) or mortgage insurance premium (FHA loans).

3. Credit score

Your credit score tells lenders about your creditworthiness, which is how likely you are to pay back a loan based on your credit history. This score provides the benchmark for your loan qualification and is one of the primary factors that determines your interest rate. Usually, the higher your credit score, the lower your interest rate.

Are there ways to qualify to borrow more?

Don’t be disappointed if you can’t initially borrow the amount you hoped you’d be able to. Remember, there are many different factors at work. The good news is that with some patience and a few small changes, you can substantially improve the amount of money that you can borrow.

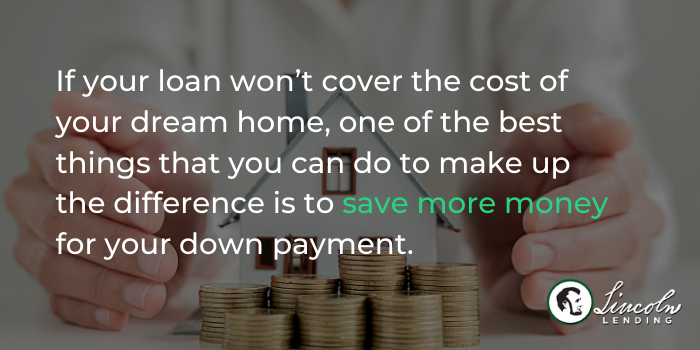

1. Put down a larger down payment

If your loan won’t cover the cost of your dream home, one of the best things that you can do to make up the difference is to save more money for your down payment. Doing so may help you qualify for a better loan. Plus, the more you put down in cash, the less you’ll have to borrow and pay back with interest.

2. Become a tactical buyer

Buying your forever home may require a long-term strategy on your part. For example, if you don’t have young children, then you can save some money by choosing a home in a transitioning neighborhood that doesn’t have an outstanding school district.

You could also consider buying a small starter home and using it to build your equity, with the intention to sell it and put it toward your forever home in a few years. Both strategies will help you find a lower-priced home so that you won’t have to borrow as much now and can put you in a stronger position to upgrade in the future.

3. Reduce your debt, even if it’s just by a little

Reducing your debt, even just by a fraction, can go a long way toward lowering your debt-to-income ratio and bumping up your credit score. Try paying off, or down, a credit card or two to help reduce your debt.

Strategize with a home loan coach

Let’s discuss how much you can afford together! Schedule a consultation with one of our home loan coaches to see what loan terms you qualify for now and make a plan to help you buy your dream home. Together, we’ll create a roadmap for reducing your debt, increasing your credit score, and/or saving more money for a down payment.